3QFY2018 Result Update | Media

February 14, 2018

Asian Granito

NEUTRAL

CMP

`519

Performance Update

Target Price

-

Y/E March (` cr)

3QFY18

3QFY17

% yoy

2QFY18

% qoq

Investment Period

12 Months

Net sales

264

248

6.4

274

(3.9)

Stock Info

EBITDA

36

34

5.6

37

(2.4)

Sector

Ceramic

Market Cap (` cr)

1,560

EBITDA margin (%)

13.7

13.8

(10bp)

13.5

21bp

Net Debt (` cr)

315

Beta

1.0

Adjusted PAT

12

13

(7.7)

16

(27.7)

52 Week High / Low

617/265

Avg. Daily Volume

40,763

Source: Company, Angel Research

Face Value (`)

10

BSE Sensex

34,300

For 3QFY2018, Asian Granito (AGL) posted results in line with our expectations

Nifty

10,540

Reuters Code

ASGI.BO

on top-line basis, however bottom-line disappointed. Revenue grew by ~6% yoy

Bloomberg Code

ASIAN.IN

(after adjusting exercise duty top-line growth grew ~13.8% ) to `264cr, driven by

Shareholding Pattern (%)

strong volume growth of ~25%. On the operating front, margins contracted by

Promoters

32.7

MF / Banks / Indian Fls

7.3

10bps yoy due to higher power (gas price rose more than 10% during the

FII / NRIs / OCBs

5.1

Indian Public / Others

55.0

quarter) and employee costs. This led to PAT de-growth of ~8% yoy to `12cr.

Abs.(%)

3m

1yr

3yr

Top-line driven by strong volume growth: The company’s top-line grew by ~6%

Sensex

3.8

21.0

19.1

AGL

5.5

88.1

326.4

yoy to `264cr (after adjusting exercise duty top-line growth grew ~13.8%) on the

back of strong volume growth (up by ~25%). In the Tiles & Quartz segment, the

company has reported ~25% & 40% volume growth respectively. However, the

Marble segment witnessed a sharp volume decline of ~37%.

Increase in power and employee costs impacted the operating margins: On the

operating front, margins contracted by 10bps yoy due to higher power (gas price

rose more than 10% during the quarter) and employee costs. This led to PAT de-

growth of ~8% yoy to `12cr.

Outlook and Valuation: We expect various initiatives taken by the government like

smart cities, housing for all by 2022, and push towards providing sanitation, to

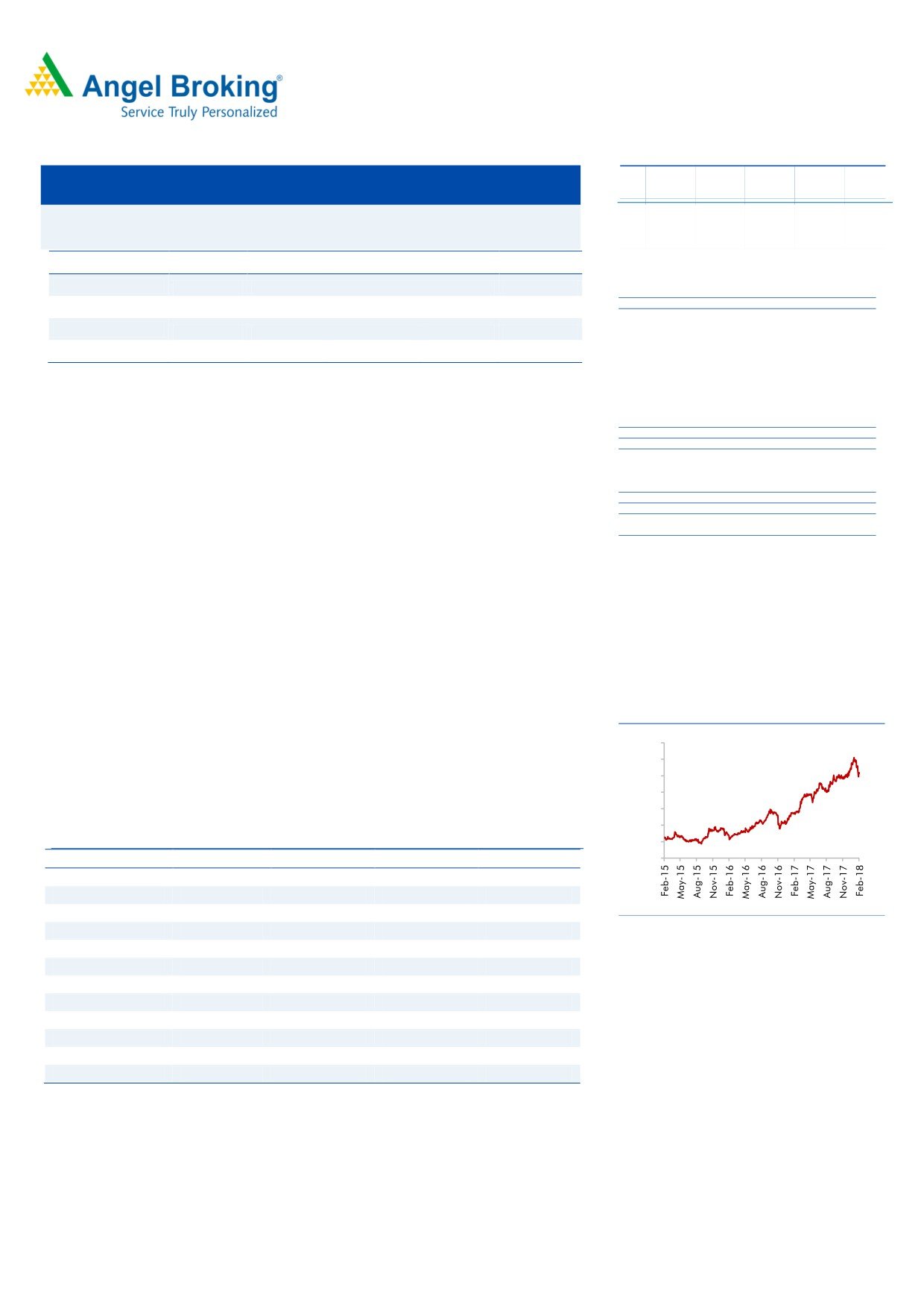

3-year price chart

further lead to creation of new demand avenues for entry level or lower priced

700

tiles (ceramic tiles). We expect AGIL to report net revenue CAGR of ~8% to

600

~`1,253cr over FY2017-19E. On bottom-line front, we expect CAGR of ~18% to

500

`55cr over FY2017-19E owing to better product mix, higher B2C sales and

400

amalgamation synergy. Currently we have neutral rating on stock.

300

200

Key financials

100

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

0

Net sales

994

1,066

1,130

1,253

% chg

18.1

7.2

6.0

10.9

Net profit

25

39

52

55

Source: Company, Angel Research

% chg

24.8

39.1

52.5

54.8

EBITDA margin (%)

9.1

11.6

13.2

12.2

EPS (`)

8.2

13.0

17.4

18.2

P/E (x)

63.0

39.9

29.7

28.5

P/BV (x)

4.3

3.9

3.4

3.1

RoE (%)

6.8

9.8

11.6

10.8

Amarjeet S Maurya

RoCE (%)

9.0

11.9

14.8

13.9

EV/Sales (x)

1.9

1.8

1.6

1.5

022-39357800 Ext: 6831

EV/EBITDA (x)

20.7

15.2

12.4

12.1

Source: Company, Angel Research, Note: CMP as of February 12, 2018

Please refer to important disclosures at the end of this report

1

Asian Granito| 3QFY2018 Result Update

Exhibit 1: 3QFY2018 Consolidated Performance

Y/E March (` cr)

3QFY18

3QFY17

% yoy

2QFY18

% qoq

9MFY18

9MFY17

% chg

Net Sales

264

248

6.4

274

(3.9)

764

731

4.5

Consumption of RM

129

122

5.9

143

(9.8)

390

386

0.9

(% of Sales)

49.0

49.2

52.2

51.0

52.8

Staff Costs

19

15

25.8

22

(13.5)

61

45

34.6

(% of Sales)

7.4

6.2

8.2

8.0

6.2

Other Expenses

79

76

3.4

72

10.1

210

207

1.8

(% of Sales)

29.9

30.7

26.1

27.5

28.3

Total Expenditure

228

214

6.5

237

(4.1)

661

638

3.6

Operating Profit

36

34

5.6

37

(2.4)

103

93

10.9

OPM

13.7

13.8

13.5

13.4

12.7

Interest

11

12

(7.9)

9

20.9

28

30

(5.5)

Depreciation

6

6

(2.0)

5

19.8

18

18

2.8

Other Income

1

0

156.7

1

(47.6)

2.41

0.6

301.7

PBT (excl. Ext Items)

20.3

16.9

20.3

24.7

(17.9)

59

46

28.5

Ext (Income)/Expense

-

-

-

-

-

PBT (incl. Ext Items)

20

17

20.3

25

(17.9)

59

46

28.5

(% of Sales)

7.7

6.8

9.0

7.7

6.2

Provision for Taxation

7

3

126.5

11

(30.7)

21

15

42.5

(% of PBT)

36.7

19.5

43.4

37

33

Reported PAT

13

14

(5.4)

14

(8.2)

37

31

21.6

PATM

4.9

5.5

5.1

4.9

4.2

Minority Interest After NP

Profit/Loss of Associate Company

(1)

(1)

2

2

2

Reported PAT

12

13

(7.7)

16

(27.7)

39

32

21.0

Source: Company, Angel Research

February 14, 2018

2

Asian Granito| 3QFY2018 Result Update

Key investment arguments

Focus on high value products

AGIL’s current vitrified sales (45%) are lower in comparison to its peers like

Somany Ceramics (50%) and Kajaria Ceramics (63-64%). Recently, AGIL has

launched various products in premium segments like Imperio, Jumbo - Double

Charge, CARARRA White, XXL - Polished Glazed Vitrified Tiles and Polished

Vitrified Tiles (Double Charge). Going forward, we expect AGIL’s profit margins to

improve due to increase in focus on higher vitrified product sales, which is a high

margin segment.

Margins to get a leg up post shift from B2B to B2C

AGIL has continuously focused on improving B2C sales from the current levels

(37% in FY17). It is expected to reach up to 50% over next 3 years following

multiple initiatives taken to increase direct interaction with customers including

strengthening distribution network, launch of exclusive brand showrooms, trade

schemes on high value products and participation in key trade exhibitions.

Further strengthening distribution network

AGIL has an extensive marketing and distribution network, comprising more than

5,780 dealers and sub-dealers. Currently, the company has 200+ exclusive dealer

showrooms, on top of which it plans to add 500 new showrooms in next 3 years.

The company also runs 16 large-format exclusive corporate display stores for

dealers and architects. Going forward, we expect the company to continue to

expand its network through dealers & sub-dealers.

February 14, 2018

3

Asian Granito| 3QFY2018 Result Update

Outlook and Valuation

We expect various initiatives taken by the government like smart cities, housing for

all by 2022, and push towards providing sanitation, to further lead to creation of

new demand avenues for entry level or lower priced tiles (ceramic tiles). We expect

AGIL to report a net revenue CAGR of ~8% to ~`1,253cr over FY2017-19E. On

bottom-line front, we expect CAGR of ~18% to `55cr over FY2017-19E owing to

better product mix, higher B2C sales and amalgamation synergy. Currently we

have neutral rating on stock.

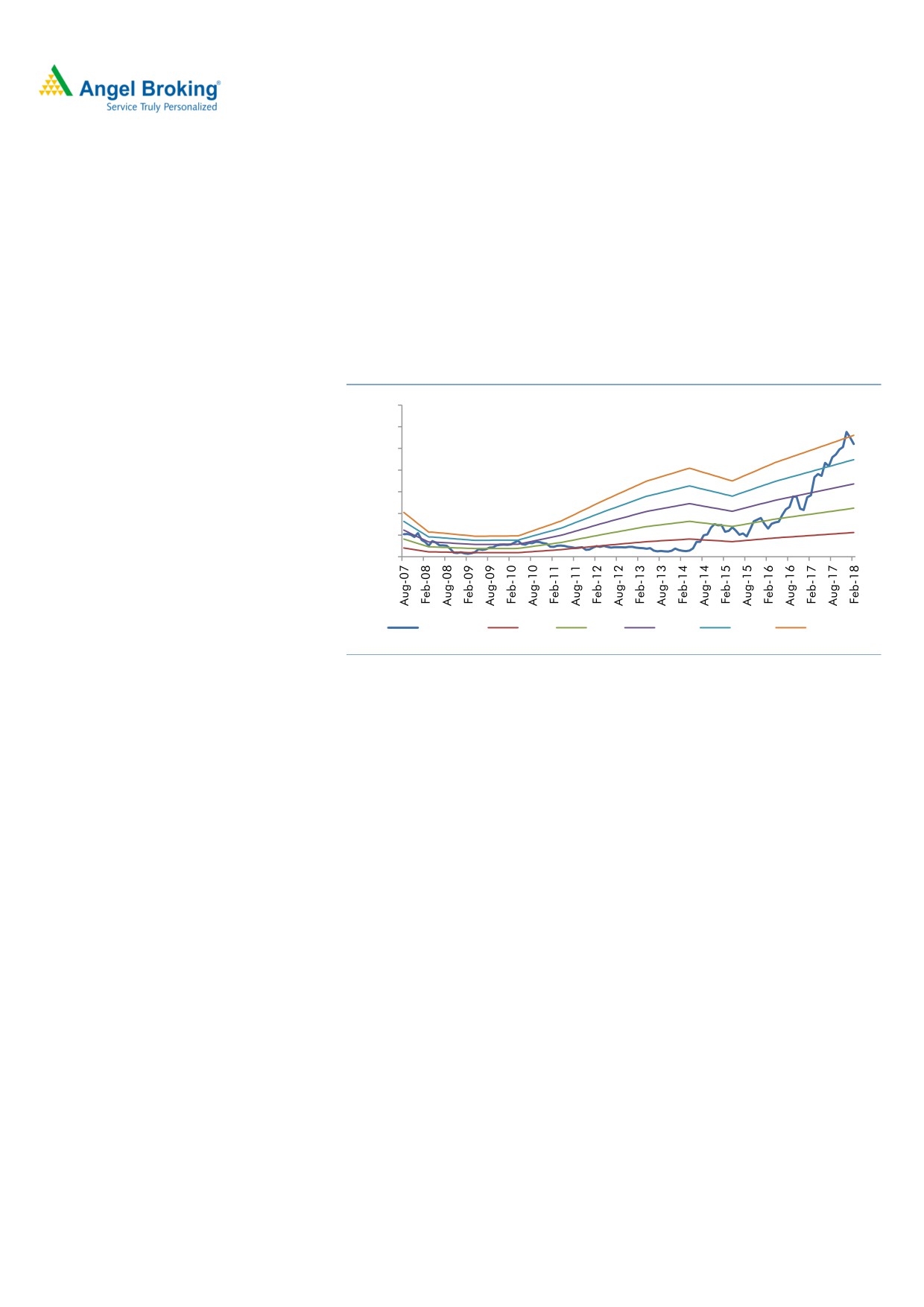

Exhibit 2: One year forward PE Chart

700

600

500

400

300

200

100

0

Share Price

4.0 X

8.0 X

12.0 X

16.0 X

20.0 X

Source: Company, Angel Research

Risks

1) Lower than expected recovery in real estate industry can impact the overall

performance (~65% revenue comes from B2B business).

2) Increase in gas prices can impact the company’s operating performance.

Company Background

Asian Granito India Limited (AGL) was established in 2000 by Mr. Kamlesh Patel

and Mr. Mukesh Patel. AGL is one of the top three Indian Ceramic Companies

engaged in the business of manufacturing, and trading of Ceramic Wall, Floor,

Vitrified Tiles, Marble & Quartz Headquartered in Gujarat. AGL has

8

manufacturing facilities in Gujarat. AGL has production of 1,00,000 sqm per day

including outsourcing. Pan India marketing & distribution network of more than

5,780 dealers and sub-dealers and over 206+ showrooms with global footprint

with exports to over 53 countries.

February 14, 2018

4

Asian Granito| 3QFY2018 Result Update

Consolidated Profit & Loss Statement

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E FY2019E

Total operating income

842

994

1,066

1,130

1,253

% chg

9.0

18.1

7.2

6.0

10.9

Total Expenditure

781

904

942

981

1,100

Cost of Materials

534

615

591

576

636

Personnel

42

59

71

90

103

Power, Oil & Fuel

131

128

141

145

160

Others Expenses

74

102

138

169

200

EBITDA

61

90

124

149

153

% chg

(5.1)

48.4

36.8

20.7

2.5

(% of Net Sales)

7.2

9.1

11.6

13.2

12.2

Depreciation& Amortization

19

28

34

35

37

EBIT

42

63

89

114

115

% chg

(1.6)

50.0

42.0

28.3

1.0

(% of Net Sales)

5.0

6.3

8.4

10.1

9.2

Interest & other Charges

23

29

39

39

36

Other Income

1

1

4

4

4

(% of PBT)

4.7

3.9

6.7

4.5

4.3

Share in profit of Associates

-

-

-

-

-

Recurring PBT

20

35

53

79

83

% chg

(11.3)

74.2

51.9

49.3

4.3

Prior Period & Extraordinary Expense/(Inc.)

-

-

-

-

-

PBT (reported)

20

35

53

79

83

Tax

6

11

13

26

27

(% of PBT)

27.9

32.2

25.2

33.0

33.0

PAT (reported)

15

24

40

53

55

Add: Share of earnings of associate

-

2

3

3

3

Less: Minority interest (MI)

-

2

3

3

3

Extraordinary Items

(1)

PAT after MI (reported)

15

25

39

52

55

% chg

1.7

70.9

57.8

34.2

4.3

(% of Net Sales)

1.7

2.5

3.7

4.6

4.4

Basic EPS (`)

4.8

8.2

13.0

17.4

18.2

Fully Diluted EPS (`)

4.8

8.2

13.0

17.4

18.2

% chg

1.7

70.9

57.8

34.2

4.3

February 14, 2018

5

Asian Granito| 3QFY2018 Result Update

Exhibit 3: Consolidated Balance Sheet

Y/E March (` cr)

FY2015

FY2016

FY2017

FY2018E

FY2019E

SOURCES OF FUNDS

Equity Share Capital

23

23

30

30

30

Reserves& Surplus

267

341

371

423

479

Shareholders Funds

290

363

401

454

509

Minority Interest

-

19

22

19

19

Total Loans

175

335

350

320

320

Deferred Tax Liability

18

30

34

30

30

Total Liabilities

483

747

807

831

885

APPLICATION OF FUNDS

Gross Block

338

603

644

694

744

Less: Acc. Depreciation

149

211

239

274

311

Net Block

188

392

405

421

433

Capital Work-in-Progress

15

6

1

6

6

Investments

11

13

17

13

13

Current Assets

438

539

679

627

694

Inventories

191

245

273

285

316

Sundry Debtors

166

197

311

220

240

Cash

15

17

19

21

25

Loans & Advances

21

30

35

56

63

Other Assets

46

50

41

45

50

Current liabilities

168

203

295

236

260

Net Current Assets

270

336

384

391

433

Deferred Tax Asset

-

-

-

-

-

Mis. Exp. not written off

-

-

-

-

-

Total Assets

483

747

807

831

885

Source: Company, Angel Research

February 14, 2018

6

Asian Granito| 3QFY2018 Result Update

Exhibit 4: Consolidated Cashflow Statement

Y/E March ((` cr)

FY2015

FY2016

FY2017

FY2018E FY2019E

Profit before tax

19

35

53

79

83

Depreciation

19

28

34

35

37

Change in Working Capital

49

(64)

(46)

(5)

(38)

Interest / Dividend (Net)

23

29

39

39

36

Direct taxes paid

(6)

(5)

(10)

(26)

(27)

Others

0

(1)

(6)

(1)

(1)

Cash Flow from Operations

104

21

65

121

90

(Inc.)/ Dec. in Fixed Assets

(30)

(224)

(42)

(47)

(50)

(Inc.)/ Dec. in Investments

2

(3)

(3)

3

-

Cash Flow from Investing

(33)

(221)

(38)

(50)

(50)

Issue of Equity

-

8

-

-

-

Inc./(Dec.) in loans

(53)

160

15

(30)

-

Dividend Paid (Incl. Tax)

-

-

(2)

-

-

Interest / Dividend (Net)

(23)

36

(39)

(39)

(36)

Cash Flow from Financing

(76)

203

(26)

(69)

(36)

Inc./(Dec.) in Cash

(4)

3

1

2

4

Opening Cash balances

19

15

17

19

21

Closing Cash balances

15

17

19

21

25

Source: Company, Angel Research

February 14, 2018

7

Asian Granito| 3QFY2018 Result Update

Exhibit 5: Key Ratios

Y/E March

FY2015

FY2016

FY2017E FY2018E FY2019E

Valuation Ratio (x)

P/E (on FDEPS)

107.6

63.0

39.9

29.7

28.5

P/CEPS

46.5

30.4

21.0

17.7

16.8

P/BV

5.4

4.3

3.9

3.4

3.1

Dividend yield (%)

0.0

0.0

0.0

0.0

0.0

EV/Sales

2.0

1.9

1.8

1.6

1.5

EV/EBITDA

28.1

20.7

15.2

12.4

12.1

EV / Total Assets

2.6

2.0

1.7

1.7

1.6

Per Share Data (Rs)

EPS (Basic)

4.8

8.2

13.0

17.4

18.2

EPS (fully diluted)

4.8

8.2

13.0

17.4

18.2

Cash EPS

11.1

17.0

24.7

29.2

30.9

DPS

0.0

0.0

0.0

0.0

0.0

Book Value

96.3

120.7

133.3

150.7

169.3

Returns (%)

ROCE

9.0

9.0

11.9

14.8

13.9

Angel ROIC (Pre-tax)

9.5

9.4

12.4

15.5

14.6

ROE

5.0

6.8

9.8

11.6

10.8

Turnover ratios (x)

Asset Turnover (Gross Block)

2.5

1.6

1.7

1.6

1.7

Inventory / Sales (days)

83

90

92

92

92

Receivables (days)

72

72

72

71

70

Payables (days)

61

57

53

52

52

Working capital cycle (ex-cash) (days)

94

105

111

111

110

Source: Company, Angel Research

February 14, 2018

8

Asian Granito| 3QFY2018 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Asian Granito

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

February 14, 2018

9

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)